library(corrr)

library(psych)

library(lavaan)

library(dplyr)

library(tidyr)

library(ggplot2)

library(haven)

library(rempsyc)

library(broom)

library(report)

library(effectsize)

library(aod)

library(readr)

library(forcats)

library(ggcorrplot)

library(caret)

library(knitr)

library(ROCR)

library(jtools)

library(xtable)

library(glmnet)

library(ggpubr)

library(lme4)

library(nlme)

library(weights)

library(miscTools)

library(systemfit)

library(multcomp)

require(ggplot2)

require(GGally)

require(reshape2)

require(lattice)

library(HLMdiag)

library(margins)

library(performance)

library(ggnewscale)

library(ggeffects)

library(ggeffects)

library(marginaleffects)

library(effects)

library(margins)

library(modelr)

library(plm)

library(effectsize)

library(aod)

library(readr)

library(tidymodels)

library(ggcorrplot)

library(glmnet)

library(ggpubr)

library(foreign)

library(AER)

library(lme4)

library(formatR)

library(pglm)

library(acqr)

library(lmtest)

library(poLCA)

library(mirt)

library(texreg)

library(gt)Device Divide

Data Analysis

In this project, I focused on analyzing how mental health relates to mobile banking adoption. I used data from the Canadian Internet Use Survey 2022, which includes questions about various digital habits, and demographics. You can find the dataset here.

For this project, I conducted a comparative analysis of two logistic regression models one for smartphone users, refered to from here on out and PHONE users and one for smart wearable users, refered to as WEAR users. Since the sampling methodology involved clustering by provinces, I considered robust standard errors for reporting the results. To build the models, I needed to conceptualize technology, in this case, m-banking adoption. Since I’m considering two different devices, I needed factors that impact m-banking decisions for both devices to be able to compare them.

This was very challenging because there are not many m-banking using smartwearable device studies! So, I broadened the scope to consider any technology adoption. This is ok to do as long as the factors are not specific to a niche context. The variables are Trust, Perceived Security, Perceived Value, and few demographic varaibles such as Age, Gender, Education and Income.

Here are my hypotheses:

- H1: The association between Trust and m-banking adoption is the same for smartphone and smart wearable users

- H2: The association between Perceived security and m-banking adoption is the same for smartphone and smart wearable users.

- H3: The association between Perceived value (measured by time savings) and m-banking adoption is the same for smartphone and smart wearable users.

- H4.1 : The association between Age and m-banking adoption is the same for smartphone and smart wearable users.

- H4.2 : The association between Gender and m-banking adoption is the same for smartphone and smart wearable users.

- H4.3 : The association between Education and m-banking adoption is the same for smartphone and smart wearable users.

- H4.4 : The association between Income and m-banking adoption is the same for smartphone and smart wearable users.

Importing Libraries

Note that not all libraries may be utilized. The most important ones are dplyr, lme4, tidyr, lavaan, ggplot2, psych, corrr, haven, poLCA and any related libraries to these.

Introducing the CIUS 2022

This dataset is very similar to CIUS 2020 from study 2. I first started by reading the entire PUMF file available.

This gives you information on how the survey was set up, why, and how things were measured. Then, I looked at the individual survey questions to see the available data, and how they were measured. In general, questions are measured numerically were answeres follow as such:

Yes : 1 No : 2

Valid Skip: 6 Don’t Know: 7 Refusal: 8 Not Stated: 9

Of course this differs question-by-question as some questions have other answer categories and some questions (which were note used in my study) asked for numerical input from the participants (like how much did you spend online last year). To help readers understand the data, I will include the question exactly as it appears in the CIUS 2022 PUMF Data Dictionary with corresponding answer choices and codes. These will be in a blue-bordered box, and will include the Variable name (on the PUMF file), Concept, Question Body and Answers. Then I will show you in R code how I’ve re-coded and used the question as a model variable. The Variables I need are as follows:

- Mobile banking adoption (

MBANK) - Province (

PRVNC) - Age Group (

AGE) - Gender (

SEX) - Education Level (

EDU) - Income Quintile (

INCOME) - User Type (

USR_TYP) - based on the following- Smartphone User (

isSmartPhone) - Smartwearable User (

isSmartWear)

- Smartphone User (

- Saved Time Because of m-banking (

EFF_TIME) - Perceived Security (

PSEC) - based on the following- Security measure: restricting access to location (

SEC_RES_LOC) - Security measure: restricting access to data (

SEC_RES_DAT) - Security check: checked security of a website (

SEC_ACC_WEBSEC) - Security check: changed privacy settings (

SEC_ACC_CHNGPRV) - Security feature: security questions (

SECOPT_QS) - Security feature: partner login (

SECOPT_PL) - Security feature: two factor authentication (

SECOPT_2FA) - Security feature: biometric (

SECOPT_BIO) - Security feature: password manager (

SECOPT_PAS)

- Security measure: restricting access to location (

- Trust in Banks (

TRST_BANK) - Family Relation Satisfaction (

FAMSAT)

The data is available in various formats. To avoid data loss, I decided to use the .dta format (SAS file). You need the haven package to read SAS files. This is how you’d read a SAS file:

data_2022 <- read_dta("data/00_CIUS2022.dta")

ds00 <- data_2022

dim(ds00)[1] 25118 342ds0 <- ds00Constructing Model Variables

- Renaming variables

- Cleaning data: delete the skips and such for both categorical and numerical variables

- Verifying that our measure of latent constructs are strong enough

Demographic Variables

Since these are not direct questions but information retrieved from other sources (such as postal codes for province), some of them do not have Skips/Don’t Know/Refusal/Not Stated answers. If they have, I have added those to the cards.

Province, Age, Sex, Education, Income:

Variable Name: PROVINCE

Concept: PROVINCE

Question Text/Note:

Information derived using postal codes.

| Answer Categories | Code |

|---|---|

| Newfoundland and Labrador | 10 |

| Prince Edward Island | 11 |

| Nova Scotia | 12 |

| New Brunswick | 13 |

| Quebec | 24 |

| Ontario | 35 |

| Manitoba | 46 |

| Saskatchewan | 47 |

| Alberta | 48 |

| British Columbia | 59 |

| Valid skip | 96 |

| Don’t know | 97 |

| Refusal | 98 |

| Not stated | 99 |

Variable Name: AGE_GRP

Concept: Age Groups - Derived variable

Question Text/Note:

Information derived from age of persons in household.

| Answer Categories | Code |

|---|---|

| 15 to 24 years | 01 |

| 25 to 34 years | 02 |

| 35 to 44 years | 03 |

| 45 to 54 years | 04 |

| 55 to 64 years | 05 |

| 65 years and over | 06 |

| Valid skip | 96 |

| Don’t know | 97 |

| Refusal | 98 |

| Not stated | 99 |

Variable Name: GENDER

Concept: Gender - Derived variable

Question Text/Note:

Refers to current gender which may be different from sex assigned at birth and may be different from what is indicated on legal documents. For data quality and confidentiality reasons, and because of the small population being measured, the dissemination of data according to ’Non binary’ Gender is not possible for this statistical program. So, this release uses a gender variable with only two categories. This variable is derived by looking at a large number of demographic characteristics from the respondent, it allows us to disseminate data on Gender that is reliable and unbiased.

| Answer Categories | Code |

|---|---|

| Male | 1 |

| Female | 2 |

| Valid skip | 6 |

| Don’t know | 7 |

| Refusal | 8 |

| Not stated | 9 |

Variable Name: EMP

Concept: Employment status - Derived variable

Question Text/Note:

| Answer Categories | Code |

|---|---|

| Employed | 1 |

| Not employed | 2 |

| Valid skip | 6 |

| Don’t know | 7 |

| Refusal | 8 |

| Not stated | 9 |

Variable Name: EDU

Concept: Highest certificate - Derived variable

Question Text/Note:

| Answer Categories | Code |

|---|---|

| High school or less | 1 |

| Some post-secondary (incl. univ certificate) | 2 |

| University degree | 3 |

| Valid skip | 6 |

| Don’t know | 7 |

| Refusal | 8 |

| Not stated | 9 |

Variable Name: HINCQUIN

Concept: Census family income quintile - Derived variable

Question Text/Note:

Information derived using HINC. In order to obtain equal weighted counts in each category, cases with incomes equal to the category cutoffs were randomly assigned to one of the two categories on either side of the cutoff.

Source Annual Income Estimates for Census Families and Individuals (T1 Family File)

| Answer Categories | Code |

|---|---|

| Quintile 1 - \leq $42,256 | 1 |

| Quintile 2 - $42,257 - $72,366 | 2 |

| Quintile 3 - $72,367 - $107,480 | 3 |

| Quintile 4 - $107,481 - $163,750 | 4 |

| Quintile 5 - > $163,750 | 5 |

| Valid skip | 6 |

| Don’t know | 7 |

| Refusal | 8 |

| Not stated | 9 |

ds0 <- ds0 %>% mutate(

ID = as.factor(pumfid),

PRVNC = case_when(

province == 10 ~ "NL",

province == 11 ~ "PEI",

province == 12 ~ "NS",

province == 13 ~ "NB",

province == 24 ~ "QC",

province == 35 ~ "ON",

province == 46 ~ "MB",

province == 47 ~ "SK",

province == 48 ~ "AB",

province == 59 ~ "BC",

.default = "default"

),

AGE = ifelse(

AGE_GRP > 10,

0,

AGE_GRP

),

SEX = case_when(

gender == 1 ~ 0, #"M",

gender == 2 ~ 1, #"F",

.default = -1 #"default" #other

),

EMP = case_when(

emp == 1 ~ 1,

emp == 2 ~ 0, #no

.default = -1

),

EDU = case_when(

edu == 1 ~ 1, #"Highschool",

edu == 2 ~ 2, #"College",

edu == 3 ~ 3, #"University",

.default = 0 #"default"

),

INCOME = case_when(

hincquin == 1 ~ 1, #"Q1",

hincquin == 2 ~ 2, #"Q2",

hincquin == 3 ~ 3, #"Q3",

hincquin == 4 ~ 4, #"Q4",

hincquin == 5 ~ 5, #"Q5",

.default = 0 #"default"

)

)Other Model Variables

Devices and Mbanking:

Variable Name: DV_010A

Concept: Devices used

Question Text/Note:

During the past three months, what devices did you use to access the Internet? Did you use: A smartphone

| Answer Categories | Code |

|---|---|

| Yes | 1 |

| No | 2 |

| Valid skip | 6 |

| Don’t know | 7 |

| Refusal | 8 |

| Not stated | 9 |

Variable Name: DV_010G

Concept: Devices used

Question Text/Note:

During the past three months, what devices did you use to access the Internet? Did you use: Internet-connected wearable smart devices

| Answer Categories | Code |

|---|---|

| Yes | 1 |

| No | 2 |

| Valid skip | 6 |

| Don’t know | 7 |

| Refusal | 8 |

| Not stated | 9 |

CIUS’s Microdata User Guide has a section (section 4. Concepts and Defintions) but it does not include a definition for Internet connected smart wearable devices. Using the internet, some examples of these smart wearable devices are:

- Smart glasses

- Smart watch

- Fitness Trackers

- Smart Shirt

- GPS devices (SGPS/GPRS Body Control)

- Bluetooth Key Trackers

- Smart Belts

- Smart Rings

- Smart Bracelets

- Virtual Reality devices

- Smart clothing

More specific to Canada, according to Ingenium.ca, the top devices are:

- Smartwatches (Apple Watch, Samsung Galaxy Watch and Fitbits)

- Fitness Trackers (Fitbit, Garmin)

- Health Monitoring Devices (continuous glucose monitors)

Also true from CIUS 2020’s report:

In addition, 14% of Canadians used Internet-connected wearable smart devices, such as a smart watch, Fit Bit or glucose monitoring device

It’s safe to assume that smart wearables most definitely include smartwatches.

Variable Name: UI_050D

Concept: Activities related to other online activities

Question Text/Note:

During the past three months, which of the following other online activities, have you done over the Internet? Have you: Conducted online banking

| Answer Categories | Code |

|---|---|

| Yes | 1 |

| No | 2 |

| Valid skip | 6 |

| Don’t know | 7 |

| Refusal | 8 |

| Not stated | 9 |

ds0 <- ds0 %>% mutate(

SMRTPHN = case_when(

DV_010A == 1 ~ 1,

DV_010A == 2 ~ 0,

.default = -1

),

SMRTWTCH = case_when(

DV_010G == 1 ~ 1,

DV_010G == 2 ~ 0,

.default = -1

),

MBANK = case_when(

UI_050D == 1 ~ 1,

UI_050D == 2 ~ 0,

.default = -1

)

)Time Saving Effects

Variable Name: UI_110E

Concept: Effects of the use of online activities

Question Text/Note:

During the past 12 months, did your use of online activities have any of the following effects? Did it: Save you time

| Answer Categories | Code |

|---|---|

| Yes | 1 |

| No | 2 |

| Valid skip | 6 |

| Don’t know | 7 |

| Refusal | 8 |

| Not stated | 9 |

ds0 <- ds0 %>% mutate(

EFF_TIME = case_when(

UI_110E == 1 ~ 1,

UI_110E == 2 ~ 0,

.default = -1

)

)And since the online activity I’m considering is mobile banking, this would be about mobile banking (more on this in my paper, as it’s not entirely true - this is a limitation).

Security

Variable Name: SP_010A

Concept: Activities carried out to manage access to personal data

Question Text/Note:

Have you carried out any of the following to manage access to your personal data over the Internet during the past 12 months? Have you: Restricted or refused access to your geographical location

| Answer Categories | Code |

|---|---|

| Yes | 1 |

| No | 2 |

| Valid skip | 6 |

| Don’t know | 7 |

| Refusal | 8 |

| Not stated | 9 |

Variable Name: SP_010B

Concept: Activities carried out to manage access to personal data

Question Text/Note:

Have you carried out any of the following to manage access to your personal data over the Internet during the past 12 months? Have you: Refused allowing the use of personal data for advertising purposes

| Answer Categories | Code |

|---|---|

| Yes | 1 |

| No | 2 |

| Valid skip | 6 |

| Don’t know | 7 |

| Refusal | 8 |

| Not stated | 9 |

Variable Name: SP_010C

Concept: Activities carried out to manage access to personal data

Question Text/Note:

Have you carried out any of the following to manage access to your personal data over the Internet during the past 12 months? Have you: Checked that the website where you provided personal data was secure

| Answer Categories | Code |

|---|---|

| Yes | 1 |

| No | 2 |

| Valid skip | 6 |

| Don’t know | 7 |

| Refusal | 8 |

| Not stated | 9 |

Variable Name: SP_010D

Concept: Activities carried out to manage access to personal data

Question Text/Note:

Have you carried out any of the following to manage access to your personal data over the Internet during the past 12 months? Have you: Changed the privacy settings on accounts or apps

| Answer Categories | Code |

|---|---|

| Yes | 1 |

| No | 2 |

| Valid skip | 6 |

| Don’t know | 7 |

| Refusal | 8 |

| Not stated | 9 |

Security Measures - Setting Up

Variable Name: SP_020A

Concept: Verified identity over the Internet

Question Text/Note:

During the past 12 months, did you enable any of the following optional security features to verify your identity when accessing accounts or applications over the Internet? Did you enable: Answers to personalized security questions

| Answer Categories | Code |

|---|---|

| Yes | 1 |

| No | 2 |

| Valid skip | 6 |

| Don’t know | 7 |

| Refusal | 8 |

| Not stated | 9 |

Variable Name: SP_020B

Concept: Verified identity over the Internet

Question Text/Note:

During the past 12 months, did you enable any of the following optional security features to verify your identity when accessing accounts or applications over the Internet? Did you enable: Partner login

| Answer Categories | Code |

|---|---|

| Yes | 1 |

| No | 2 |

| Valid skip | 6 |

| Don’t know | 7 |

| Refusal | 8 |

| Not stated | 9 |

Variable Name: SP_020C

Concept: Verified identity over the Internet

Question Text/Note:

During the past 12 months, did you enable any of the following optional security features to verify your identity when accessing accounts or applications over the Internet? Did you enable: Two-factor authentication or two-step verification

| Answer Categories | Code |

|---|---|

| Yes | 1 |

| No | 2 |

| Valid skip | 6 |

| Don’t know | 7 |

| Refusal | 8 |

| Not stated | 9 |

Variable Name: SP_020D

Concept: Verified identity over the Internet

Question Text/Note:

During the past 12 months, did you enable any of the following optional security features to verify your identity when accessing accounts or applications over the Internet? Did you enable: Biometric security features for online functions

| Answer Categories | Code |

|---|---|

| Yes | 1 |

| No | 2 |

| Valid skip | 6 |

| Don’t know | 7 |

| Refusal | 8 |

| Not stated | 9 |

Variable Name: SP_020E

Concept: Verified identity over the Internet

Question Text/Note:

During the past 12 months, did you enable any of the following optional security features to verify your identity when accessing accounts or applications over the Internet? Did you enable: Password manager program

| Answer Categories | Code |

|---|---|

| Yes | 1 |

| No | 2 |

| Valid skip | 6 |

| Don’t know | 7 |

| Refusal | 8 |

| Not stated | 9 |

ds0 <- ds0 %>% mutate(

SEC_RES_LOC = case_when(

SP_010A == 1 ~ 1,

SP_010A == 2 ~ 0,

.default = -1

),

SEC_RES_DAT = case_when(

SP_010B == 1 ~ 1,

SP_010B == 2 ~ 0,

.default = -1

),

SEC_ACC_WEBSEC = case_when(

SP_010C == 1 ~ 1,

SP_010C == 2 ~ 0,

.default = -1

),

SEC_ACC_CHNGPRV = case_when(

SP_010D == 1 ~ 1,

SP_010D == 2 ~ 0,

.default = -1

),

SECOPT_QS = case_when(

SP_020A == 1 ~ 1,

SP_020A == 2 ~ 0,

.default = -1

),

SECOPT_PL = case_when(

SP_020B == 1 ~ 1,

SP_020B == 2 ~ 0,

.default = -1

),

SECOPT_2FA = case_when(

SP_020C == 1 ~ 1,

SP_020C == 2 ~ 0,

.default = -1

),

SECOPT_BIO = case_when(

SP_020D == 1 ~ 1,

SP_020D == 2 ~ 0,

.default = -1

),

SECOPT_PAS = case_when(

SP_020E == 1 ~ 1,

SP_020E == 2 ~ 0,

.default = -1

)

)Trust In Banks/Financial Institutes

Variable Name: SP_040B

Concept: Personal information - Trust in organizations

Question Text/Note:

In general, on a scale from 1 to 5 where 1 means “cannot be trusted at all” and 5 means “can be trusted completely”, to what extent do you trust the following organizations with your personal information? Would you say: b. Banking or other financial institutions

| Answer Categories | Code |

|---|---|

| 1 - Cannot be trusted at all | 1 |

| 2 | 2 |

| 3 - Neutral | 3 |

| 4 | 4 |

| 5 - Can be trusted completely | 5 |

| Valid skip | 6 |

| Don’t know | 7 |

| Refusal | 8 |

| Not stated | 9 |

ds0 <- ds0 %>% mutate(

TRST_BANK = case_when(

SP_040B == 1 ~ 1, #cannot be trusted

SP_040B == 2 ~ 2,

SP_040B == 3 ~ 3, #neutral

SP_040B == 4 ~ 4,

SP_040B == 5 ~ 5, #totally trusted

.default = 0

)

)Selecting only the useful columns:

ds_useful <- ds0 %>% dplyr::select(wtpg:TRST_BANK)I have to make sure that online banking is actually capturing mobile banking, so, people must be smartphone users:

ds_mobilebank <- ds_useful %>% filter(SMRTPHN == 1)dim(ds_mobilebank)[1] 20136 22Looking at the data,

glimpse(ds_mobilebank)Rows: 20,136

Columns: 22

$ wtpg <dbl> 1264.0837, 3413.0468, 585.5445, 378.8767, 4060.0513, 7…

$ ID <fct> 100001, 100002, 100004, 100005, 100007, 100008, 100009…

$ PRVNC <chr> "QC", "MB", "QC", "SK", "QC", "QC", "AB", "ON", "SK", …

$ AGE <dbl> 3, 1, 5, 4, 2, 4, 6, 3, 3, 6, 2, 3, 4, 5, 4, 5, 5, 4, …

$ SEX <dbl> 1, 0, 0, 0, 1, 0, 0, 1, 1, 0, 1, 1, 1, 0, 1, 0, 0, 0, …

$ EMP <dbl> 1, 0, 0, 1, 1, 1, 0, 1, -1, 0, 1, 1, 1, -1, 1, 1, 0, 1…

$ EDU <dbl> 3, 1, 2, 1, 2, 2, 2, 2, 0, 3, 3, 3, 3, 2, 1, 3, 3, 2, …

$ INCOME <dbl> 2, 2, 4, 2, 2, 5, 5, 5, 5, 4, 3, 4, 3, 3, 1, 4, 2, 4, …

$ SMRTPHN <dbl> 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, …

$ SMRTWTCH <dbl> 0, 0, 0, 0, 1, 0, 0, 0, 1, 1, 0, 0, 0, 0, 0, 0, 0, 0, …

$ MBANK <dbl> 1, 0, 1, 0, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, …

$ EFF_TIME <dbl> 0, 0, 1, 0, 0, 1, 1, 0, 1, 1, 1, 0, 1, 1, 0, 1, 0, 1, …

$ SEC_RES_LOC <dbl> 1, 0, 1, 0, 0, 0, 0, 1, -1, 0, 1, 1, 1, 0, 1, 1, 0, 0,…

$ SEC_RES_DAT <dbl> 1, 0, 1, 0, 0, 0, 1, 0, -1, 0, 1, 1, 1, 0, 1, 1, 0, 0,…

$ SEC_ACC_WEBSEC <dbl> 1, 0, 0, 0, 1, 0, 1, 0, -1, 0, 0, 0, 0, 0, 1, 1, 0, 0,…

$ SEC_ACC_CHNGPRV <dbl> 1, 0, 1, 0, 0, 0, 1, 0, -1, 0, 1, 0, 1, 0, 1, 1, 0, 0,…

$ SECOPT_QS <dbl> 1, 0, 1, 0, 0, 0, 1, 1, -1, 1, 1, 0, 0, 1, 1, 1, 0, 1,…

$ SECOPT_PL <dbl> 1, 0, 0, 0, 0, 0, 0, 0, -1, 0, 0, 0, 1, 0, 1, 0, 0, 1,…

$ SECOPT_2FA <dbl> 1, 0, 1, 0, 0, 0, 0, 1, -1, 1, 1, 1, 1, 1, 1, 1, 0, 1,…

$ SECOPT_BIO <dbl> 0, 0, 0, 0, 1, 0, 1, 0, -1, 0, 1, 1, 0, 0, 1, 1, 0, 1,…

$ SECOPT_PAS <dbl> 1, 0, 0, 0, 0, 0, 0, 0, -1, 0, 1, 1, 0, 0, 1, 1, 0, 0,…

$ TRST_BANK <dbl> 3, 3, 3, 3, 3, 4, 3, 3, 0, 5, 4, 4, 3, 3, 3, 4, 4, 5, …I see there are some -1 values and some values that don’t make sense. Drop these. The data is large enough such that 100 rows won’t affect the analysis.

cleaned_ds <- ds_mobilebank %>% filter(

!is.na(AGE) &

SEX != -1 &

EDU != -1 &

EDU != 0 &

INCOME != -1 &

SMRTWTCH != -1 &

MBANK != -1 &

EFF_TIME != -1 &

SEC_RES_LOC != -1 &

SEC_RES_DAT != -1 &

SEC_ACC_WEBSEC != -1 &

SEC_ACC_CHNGPRV != -1 &

SECOPT_QS != -1 &

SECOPT_PL != -1 &

SECOPT_2FA != -1 &

SECOPT_BIO != -1 &

SECOPT_PAS != -1 &

TRST_BANK != -1 &

TRST_BANK != 0

)dim(cleaned_ds)[1] 18552 22Saving this in a database called wrk_ds (working database):

wrk_ds <- cleaned_dsPerceived Security Measurement

Since there is no perceived security measure I need to define it as a latent variable. In the CIUS2022, there’s no single, direct question asking:

How secure do you think mobile banking is?

That means “Perceived Security” isn’t directly measured. However, we have multiple related questions (e.g., about data protection, privacy, security measures, etc.). These indirect items are observable variables that reflect an unobservable (latent) concept: the user’s overall perception of security.

I use Confirmatory Factor Analysis (CFA) to test if these items really reflect one underlying factor, i.e., PSEC. This increases measurement reliability. Here are the steps of CFA:

Step 1. Reliability Check

Using Cronbach’s Alpha, I check the internal consistency of the items. Usually, if \alpha > 0.7, the items are measuring the same idea.

alph <- psych::alpha(wrk_ds[, c("SEC_RES_LOC", "SEC_RES_DAT", "SEC_ACC_WEBSEC", "SEC_ACC_CHNGPRV",

"SECOPT_QS", "SECOPT_PL", "SECOPT_2FA",

"SECOPT_BIO", "SECOPT_PAS")])

alph$total$raw_alpha[1] 0.8103267Which means the measurement is strong.

Step 2. Exploratory Factor Check

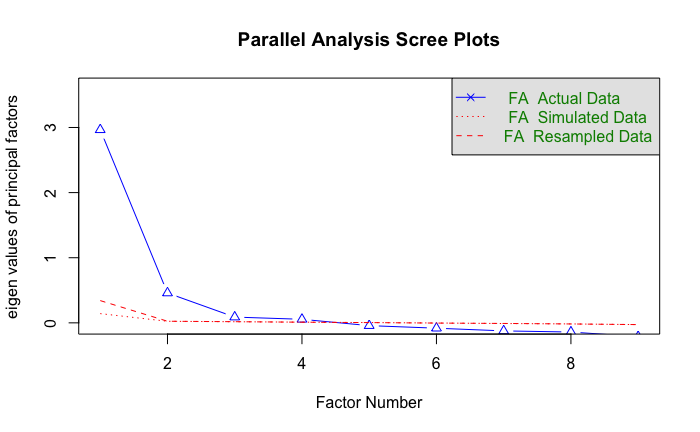

With Parallel Analysis, I can decide how many factors to extract.

fa.parallel(wrk_ds[, c("SEC_RES_LOC", "SEC_RES_DAT", "SEC_ACC_WEBSEC", "SEC_ACC_CHNGPRV",

"SECOPT_QS", "SECOPT_PL", "SECOPT_2FA", "SECOPT_BIO", "SECOPT_PAS")],

fa = "fa")

Note: the eighenvalue on the y-axis is basically the varaince each factor explains

From a parallel scree plot, you should look for an “elbow” - this is where the curve changes direction, which looks like 2 here. Parallel analysis suggests 2 separate factors. That is, it could be that the factors I’m looking at are actually describing two different latent ideas:

- Maybe security measures like questions, 2FA, biometrics

- and security concerns overall, like not allowing access to location or data

However, I still think they’re basically both perceptions of security of an app. You only do these things if you think the app is not secure or you’re worried about security. So, I’ll keep these factors and decide if something should be combined or dropped from CFA results.

Step 3. Confirmatory Factor Analysis

The mathematical model is

X_i = \lambda_i PSEC_i + \epsilon_i

Where X_i’s are the observed variables, \lambda_i is factor loading of varaible i and \epsilon is the error term. This is as if asking “can all 9 items be explained by 1 variable (PSEC)?”. I’m adding covariances to improve the model fit. How did I decide how to add covariates (this notation \sim\sim)? Trial and error, tbh! But also, mostly intuitive. The questions about security measures like setting up 2FA, questions, biometrics, password managers and partner login are all kind of related (to the same idea of “setting up and using security measures/features”). They have the same context on CIUS questionnairs, too. Similarly, the data and location access are kind of about the same idea: they’re both restrictions on what is shared about you. Lastly, changing privacy and checking a website’s security is are both activities that are not part of security features. There’s no set up, and all websites and apps have to allow you to be able to change privacy settings and you can check any website.

f1 <- '

f =~ SEC_RES_LOC + SEC_RES_DAT + SEC_ACC_WEBSEC + SEC_ACC_CHNGPRV + SECOPT_QS + SECOPT_PL + SECOPT_2FA + SECOPT_BIO + SECOPT_PAS

# Adding covariances between related error terms (based on modindices)

SEC_RES_LOC ~~ SEC_RES_DAT

SECOPT_QS ~~ SECOPT_2FA

SECOPT_BIO ~~ SECOPT_PAS

SEC_ACC_WEBSEC ~~ SEC_ACC_CHNGPRV

SECOPT_QS ~~ SECOPT_PL

'

compatibility_fac <- cfa(f1, data = wrk_ds, std.lv = TRUE)

summary(compatibility_fac, fit.measures = TRUE, standardized = TRUE)lavaan 0.6.16 ended normally after 43 iterations

Estimator ML

Optimization method NLMINB

Number of model parameters 23

Number of observations 18552

Model Test User Model:

Test statistic 1328.000

Degrees of freedom 22

P-value (Chi-square) 0.000

Model Test Baseline Model:

Test statistic 42055.218

Degrees of freedom 36

P-value 0.000

User Model versus Baseline Model:

Comparative Fit Index (CFI) 0.969

Tucker-Lewis Index (TLI) 0.949

Loglikelihood and Information Criteria:

Loglikelihood user model (H0) -93888.613

Loglikelihood unrestricted model (H1) -93224.613

Akaike (AIC) 187823.227

Bayesian (BIC) 188003.278

Sample-size adjusted Bayesian (SABIC) 187930.185

Root Mean Square Error of Approximation:

RMSEA 0.057

90 Percent confidence interval - lower 0.054

90 Percent confidence interval - upper 0.059

P-value H_0: RMSEA <= 0.050 0.000

P-value H_0: RMSEA >= 0.080 0.000

Standardized Root Mean Square Residual:

SRMR 0.034

Parameter Estimates:

Standard errors Standard

Information Expected

Information saturated (h1) model Structured

Latent Variables:

Estimate Std.Err z-value P(>|z|) Std.lv Std.all

f =~

SEC_RES_LOC 0.274 0.004 74.861 0.000 0.274 0.581

SEC_RES_DAT 0.300 0.004 82.428 0.000 0.300 0.627

SEC_ACC_WEBSEC 0.281 0.004 70.897 0.000 0.281 0.564

SEC_ACC_CHNGPR 0.336 0.004 88.679 0.000 0.336 0.673

SECOPT_QS 0.258 0.004 65.258 0.000 0.258 0.523

SECOPT_PL 0.219 0.004 58.760 0.000 0.219 0.466

SECOPT_2FA 0.275 0.003 81.371 0.000 0.275 0.620

SECOPT_BIO 0.221 0.004 58.219 0.000 0.221 0.462

SECOPT_PAS 0.217 0.004 55.881 0.000 0.217 0.446

Covariances:

Estimate Std.Err z-value P(>|z|) Std.lv Std.all

.SEC_RES_LOC ~~

.SEC_RES_DAT 0.059 0.001 40.627 0.000 0.059 0.414

.SECOPT_QS ~~

.SECOPT_2FA 0.026 0.001 19.955 0.000 0.026 0.181

.SECOPT_BIO ~~

.SECOPT_PAS 0.033 0.002 21.891 0.000 0.033 0.180

.SEC_ACC_WEBSEC ~~

.SEC_ACC_CHNGPR 0.020 0.002 13.119 0.000 0.020 0.131

.SECOPT_QS ~~

.SECOPT_PL 0.021 0.001 14.773 0.000 0.021 0.119

Variances:

Estimate Std.Err z-value P(>|z|) Std.lv Std.all

.SEC_RES_LOC 0.147 0.002 80.302 0.000 0.147 0.663

.SEC_RES_DAT 0.139 0.002 76.666 0.000 0.139 0.607

.SEC_ACC_WEBSEC 0.169 0.002 79.760 0.000 0.169 0.682

.SEC_ACC_CHNGPR 0.137 0.002 70.015 0.000 0.137 0.547

.SECOPT_QS 0.176 0.002 83.349 0.000 0.176 0.726

.SECOPT_PL 0.173 0.002 88.126 0.000 0.173 0.783

.SECOPT_2FA 0.121 0.002 77.426 0.000 0.121 0.615

.SECOPT_BIO 0.180 0.002 88.309 0.000 0.180 0.787

.SECOPT_PAS 0.190 0.002 88.964 0.000 0.190 0.802

f 1.000 1.000 1.000For CFA, this is how you’d interpret the results:

| Metric | Desired Threshold | Description |

|---|---|---|

| CFI (Comparative Fit Index) | > 0.90 | Higher is better fit |

| TLI (Tucker-Lewis Index) | > 0.90 | Higher is better fit |

| RMSEA (Root Mean Square Error of Approx.) | < 0.08 or ideally < 0.05 | Lower is better (error) |

| SRMR (Standardized Root Mean Residual) | < 0.08 | Lower is better |

The more of these “checkboxes” your summary output checks, the better the fit for the factor. Factor loadings are about how strongly each factor represents/reflects the latent factor. The higher the values the better (and significant).

My results are excellent for now, but, it’s also good to check for residuals and correlations:

Step 4. Are Items Correlated?

modindices(compatibility_fac, sort = TRUE, minimum.value = 10) lhs op rhs mi epc sepc.lv sepc.all sepc.nox

53 SECOPT_PL ~~ SECOPT_PAS 169.942 0.018 0.018 0.100 0.100

54 SECOPT_2FA ~~ SECOPT_BIO 128.215 0.014 0.014 0.092 0.092

51 SECOPT_PL ~~ SECOPT_2FA 115.978 0.014 0.014 0.096 0.096

32 SEC_RES_DAT ~~ SEC_ACC_WEBSEC 111.173 0.012 0.012 0.081 0.081

52 SECOPT_PL ~~ SECOPT_BIO 92.814 0.013 0.013 0.074 0.074

46 SEC_ACC_CHNGPRV ~~ SECOPT_2FA 86.313 -0.012 -0.012 -0.090 -0.090

33 SEC_RES_DAT ~~ SEC_ACC_CHNGPRV 82.720 0.011 0.011 0.077 0.077

26 SEC_RES_LOC ~~ SEC_ACC_CHNGPRV 63.660 0.009 0.009 0.064 0.064

28 SEC_RES_LOC ~~ SECOPT_PL 58.695 -0.009 -0.009 -0.055 -0.055

45 SEC_ACC_CHNGPRV ~~ SECOPT_PL 56.901 -0.010 -0.010 -0.066 -0.066

30 SEC_RES_LOC ~~ SECOPT_BIO 46.796 -0.008 -0.008 -0.048 -0.048

41 SEC_ACC_WEBSEC ~~ SECOPT_2FA 38.361 -0.008 -0.008 -0.054 -0.054

35 SEC_RES_DAT ~~ SECOPT_PL 35.212 -0.007 -0.007 -0.044 -0.044

55 SECOPT_2FA ~~ SECOPT_PAS 32.752 0.007 0.007 0.046 0.046

36 SEC_RES_DAT ~~ SECOPT_2FA 30.066 -0.006 -0.006 -0.043 -0.043

31 SEC_RES_LOC ~~ SECOPT_PAS 25.153 -0.006 -0.006 -0.035 -0.035

38 SEC_RES_DAT ~~ SECOPT_PAS 23.792 -0.006 -0.006 -0.035 -0.035

42 SEC_ACC_WEBSEC ~~ SECOPT_BIO 22.575 -0.007 -0.007 -0.038 -0.038

43 SEC_ACC_WEBSEC ~~ SECOPT_PAS 19.748 -0.006 -0.006 -0.035 -0.035

37 SEC_RES_DAT ~~ SECOPT_BIO 18.991 -0.005 -0.005 -0.032 -0.032

34 SEC_RES_DAT ~~ SECOPT_QS 12.791 -0.004 -0.004 -0.026 -0.026

50 SECOPT_QS ~~ SECOPT_PAS 11.720 0.005 0.005 0.026 0.026A few modification indeces are quite large, indicating these variables are highly correlated. So, it’s a good idea to add a covariance for them to the model. However, adding too much risks complicating the model and potentially overfitting. Since my analysis so far shows strong fit (above 90% CFI), I stop here. However, there’s room for improvement!

Step 5. Check Sample-sized control RMSEA

Since my sample size is quite large, the RMSEA is affected. In fact, all the metrics (especially \chi^2) are. So, I’ll calculate the sample-sized normalized RMSEA:

fitmeasures(compatibility_fac, "rmsea") / sqrt(18552)rmsea

0 And check the reliability of the model:

# reliability(compatibility_fac) --- 82%Step 6. Subgroup Analysis

Before we define PSEC, I have to figure out how many different categories I want. The smallest would be 2: high and low. I want to check for unobserved subgroups/subclasses. This is called Latent Class Analysis (LCA). Since the values for the items had 0’s in them, I have to add 1’s to everything (required for poLCA).

wrk_ds[, c("SEC_RES_LOC", "SEC_RES_DAT", "SEC_ACC_WEBSEC", "SEC_ACC_CHNGPRV",

"SECOPT_QS", "SECOPT_PL", "SECOPT_2FA", "SECOPT_BIO", "SECOPT_PAS")] <-

wrk_ds[, c("SEC_RES_LOC", "SEC_RES_DAT", "SEC_ACC_WEBSEC", "SEC_ACC_CHNGPRV",

"SECOPT_QS", "SECOPT_PL", "SECOPT_2FA", "SECOPT_BIO", "SECOPT_PAS")] + 1

form <- cbind(SEC_RES_LOC, SEC_RES_DAT, SEC_ACC_WEBSEC, SEC_ACC_CHNGPRV,

SECOPT_QS, SECOPT_PL, SECOPT_2FA, SECOPT_BIO, SECOPT_PAS) ~ 1

# Run LCA with 2 latent classes

lca_model <- poLCA(form, data = wrk_ds, nclass = 2, maxiter = 5000)Conditional item response (column) probabilities,

by outcome variable, for each class (row)

$SEC_RES_LOC

Pr(1) Pr(2)

class 1: 0.6822 0.3178

class 2: 0.1056 0.8944

$SEC_RES_DAT

Pr(1) Pr(2)

class 1: 0.7381 0.2619

class 2: 0.1067 0.8933

$SEC_ACC_WEBSEC

Pr(1) Pr(2)

class 1: 0.8797 0.1203

class 2: 0.3350 0.6650

$SEC_ACC_CHNGPRV

Pr(1) Pr(2)

class 1: 0.8775 0.1225

class 2: 0.2212 0.7788

$SECOPT_QS

Pr(1) Pr(2)

class 1: 0.7263 0.2737

class 2: 0.2124 0.7876

$SECOPT_PL

Pr(1) Pr(2)

class 1: 0.9084 0.0916

class 2: 0.5167 0.4833

$SECOPT_2FA

Pr(1) Pr(2)

class 1: 0.5936 0.4064

class 2: 0.0585 0.9415

$SECOPT_BIO

Pr(1) Pr(2)

class 1: 0.8906 0.1094

class 2: 0.4840 0.5160

$SECOPT_PAS

Pr(1) Pr(2)

class 1: 0.8515 0.1485

class 2: 0.4569 0.5431

Estimated class population shares

0.3951 0.6049

Predicted class memberships (by modal posterior prob.)

0.3843 0.6157

=========================================================

Fit for 2 latent classes:

=========================================================

number of observations: 18552

number of estimated parameters: 19

residual degrees of freedom: 492

maximum log-likelihood: -93737.84

AIC(2): 187513.7

BIC(2): 187662.4

G^2(2): 9189.15 (Likelihood ratio/deviance statistic)

X^2(2): 17134.16 (Chi-square goodness of fit)

summary(lca_model) Length Class Mode

llik 1 -none- numeric

attempts 1 -none- numeric

probs.start 9 -none- list

probs 9 -none- list

probs.se 9 -none- list

P.se 2 -none- numeric

posterior 37104 -none- numeric

predclass 18552 -none- numeric

P 2 -none- numeric

numiter 1 -none- numeric

probs.start.ok 1 -none- logical

coeff 1 -none- logical

coeff.se 1 -none- logical

coeff.V 1 -none- logical

eflag 1 -none- logical

npar 1 -none- numeric

aic 1 -none- numeric

bic 1 -none- numeric

Nobs 1 -none- numeric

Chisq 1 -none- numeric

predcell 11 data.frame list

Gsq 1 -none- numeric

y 9 data.frame list

x 1 data.frame list

N 1 -none- numeric

maxiter 1 -none- numeric

resid.df 1 -none- numeric

time 1 difftime numeric

call 5 -none- call Essentially, I’m grouping people into classes based on their security attitudes using the 9 items that I have. Let’s check the 2 classes results. How to interpret the results:

- First, Pr(1) is probability the person in class x picks 1 for an item (1 here is the previous 0). So:

$SEC_RES_LOC

Pr(1), class 1: 0.68

Pr(2), class 2: 0.11

Means people in class 1 are more likely to not restrict their location (SEC_RES_LOC = 0 has a higher chance in class 1). This can just be people with high and low security tolerance. The Estimated class population shares for classes are very close to the prediction of my model, i.e., Predicted class memberships (by modal posterior prob.). This means these are very good estimates. The fit statistics shows: AIC, BIC, deviance, and \chi^2.

Now let’s try for 2,3 and 4 classes and pick the best - using AIC/BIC (lower = better fit):

invisible(capture.output({lca_2 <- poLCA(form, data = wrk_ds, nclass = 2)}))

invisible(capture.output({lca_3 <- poLCA(form, data = wrk_ds, nclass = 3)}))

invisible(capture.output({lca_4 <- poLCA(form, data = wrk_ds, nclass = 4)}))

# Compare AIC and BIC

data.frame(

Classes = 2:4,

AIC = c(lca_2$aic, lca_3$aic, lca_4$aic),

BIC = c(lca_2$bic, lca_3$bic, lca_4$bic)

) Classes AIC BIC

1 2 187513.7 187662.4

2 3 183851.6 184078.7

3 4 180666.1 180971.4This is telling me PSEC should have 4 levels.

Step 7. Calculate Perceived Security

Another way to define PSEC is to use Item Response Theory (1 parameter logistic model, Rasch Model). This will give a continous value for PSEC, which is preferrable for my analysis. Each item shares the same slope and I estimate

P(Y_{ij} = 1) = \frac{1}{1 + e^{PSEC_j - b_i}}

Where PSEC_j is person j’s perceived security and b_i is item i’s threshold. The idea is of b_i is: how hard is it for someone to agree with something. So, in my example, how high/low does the person’s security perception have to be to skip setting up 2FA/set up 2FA.

Note: IF PSEC = b, then the person has a 50-50 chance of agreeing.

Bottom line:

- If an item has high threshold, only those with high perceived security agree with it.

- If an item has low thresholds, most agree with.

So, let’s define PSEC:

# Run a 1-parameter logistic model (Rasch Model)

irt_model <- mirt(wrk_ds[, c("SEC_RES_LOC", "SEC_RES_DAT", "SEC_ACC_WEBSEC",

"SEC_ACC_CHNGPRV", "SECOPT_QS", "SECOPT_PL",

"SECOPT_2FA", "SECOPT_BIO", "SECOPT_PAS")], 1, itemtype="Rasch")

Iteration: 1, Log-Lik: -94814.100, Max-Change: 0.40153

Iteration: 2, Log-Lik: -93680.902, Max-Change: 0.41232

Iteration: 3, Log-Lik: -93047.348, Max-Change: 0.36846

Iteration: 4, Log-Lik: -92734.044, Max-Change: 0.29365

Iteration: 5, Log-Lik: -92591.472, Max-Change: 0.21441

Iteration: 6, Log-Lik: -92529.943, Max-Change: 0.14683

Iteration: 7, Log-Lik: -92504.107, Max-Change: 0.09617

Iteration: 8, Log-Lik: -92493.300, Max-Change: 0.06119

Iteration: 9, Log-Lik: -92488.690, Max-Change: 0.03822

Iteration: 10, Log-Lik: -92486.647, Max-Change: 0.02357

Iteration: 11, Log-Lik: -92485.693, Max-Change: 0.01445

Iteration: 12, Log-Lik: -92485.221, Max-Change: 0.00882

Iteration: 13, Log-Lik: -92484.970, Max-Change: 0.00567

Iteration: 14, Log-Lik: -92484.829, Max-Change: 0.00316

Iteration: 15, Log-Lik: -92484.756, Max-Change: 0.00192

Iteration: 16, Log-Lik: -92484.712, Max-Change: 0.00125

Iteration: 17, Log-Lik: -92484.685, Max-Change: 0.00070

Iteration: 18, Log-Lik: -92484.670, Max-Change: 0.00040

Iteration: 19, Log-Lik: -92484.661, Max-Change: 0.00028

Iteration: 20, Log-Lik: -92484.655, Max-Change: 0.00015

Iteration: 21, Log-Lik: -92484.652, Max-Change: 0.00009# Extract person-level scores (PSEC)

wrk_ds$PSEC <- fscores(irt_model)This is a 1-factor model (PSEC). We find the factor scores (fscores()), otherwise known as latent trat scores, which estimate each person’s position on the latent construct (basically, each person’s PSEC score). Scores are usually centered around 0, and the more negative values are lower scores.

coef(irt_model, simplify=TRUE)$items

a1 d g u

SEC_RES_LOC 1 1.022 0 1

SEC_RES_DAT 1 0.867 0 1

SEC_ACC_WEBSEC 1 -0.348 0 1

SEC_ACC_CHNGPRV 1 0.078 0 1

SECOPT_QS 1 0.483 0 1

SECOPT_PL 1 -1.113 0 1

SECOPT_2FA 1 1.483 0 1

SECOPT_BIO 1 -0.937 0 1

SECOPT_PAS 1 -0.735 0 1

$means

F1

0

$cov

F1

F1 3.093Summary statistics of PSEC values:

summary(wrk_ds$PSEC) F1

Min. :-2.8540382

1st Qu.:-1.3479926

Median : 0.1676207

Mean : 0.0009833

3rd Qu.: 1.2059331

Max. : 2.7349158 Similar to this, but much easier - since I already used lavaan to do CFA, you can just use the same package to calculate the PSEC values for users. This is what I will use for the paper:

wrk_ds$PSEC <- lavPredict(compatibility_fac)

summary(wrk_ds$PSEC) f

Min. :-1.5300

1st Qu.:-0.7069

Median : 0.1029

Mean : 0.0000

3rd Qu.: 0.7779

Max. : 1.3023 Build Datasets for Modeling

So, I need 3 different datasets for modeling:

- Full Data: includes everything

- PHON-only Data: only smartphone users

- WEAR-only Data: only smartwear users

Let’s separate the data:

wrk_ds <- wrk_ds %>% mutate(

isSmartPhone = if_else(

SMRTPHN == 1,

1,

0

),

isSmartWear = if_else(

SMRTWTCH == 1,

1,

0

)

)Some Visualizations

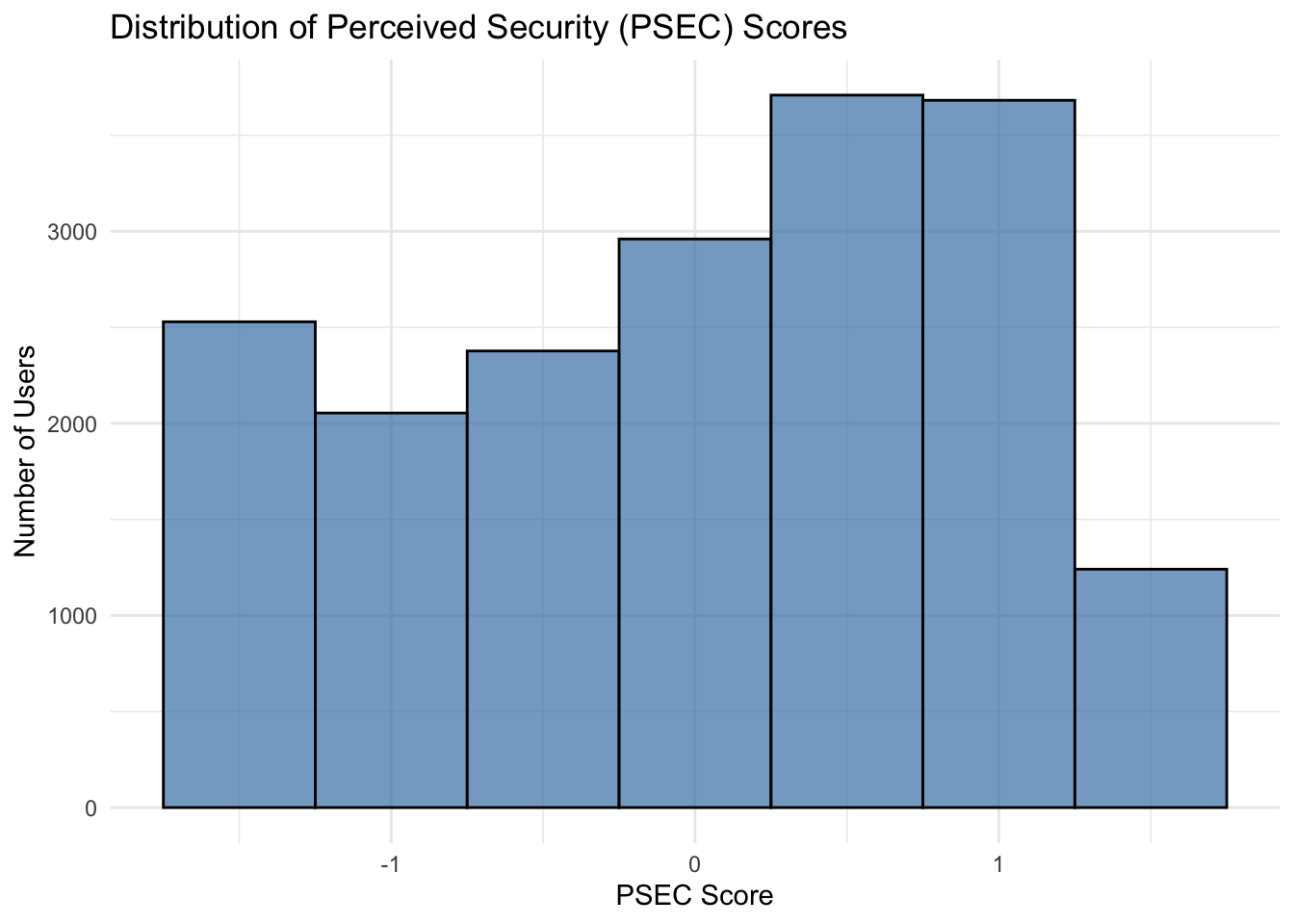

ggplot(wrk_ds, aes(x = PSEC)) +

geom_histogram(binwidth = 0.5, fill = "steelblue", color = "black", alpha = 0.7) +

labs(title = "Distribution of Perceived Security (PSEC) Scores",

x = "PSEC Score",

y = "Number of Users") +

theme_minimal()

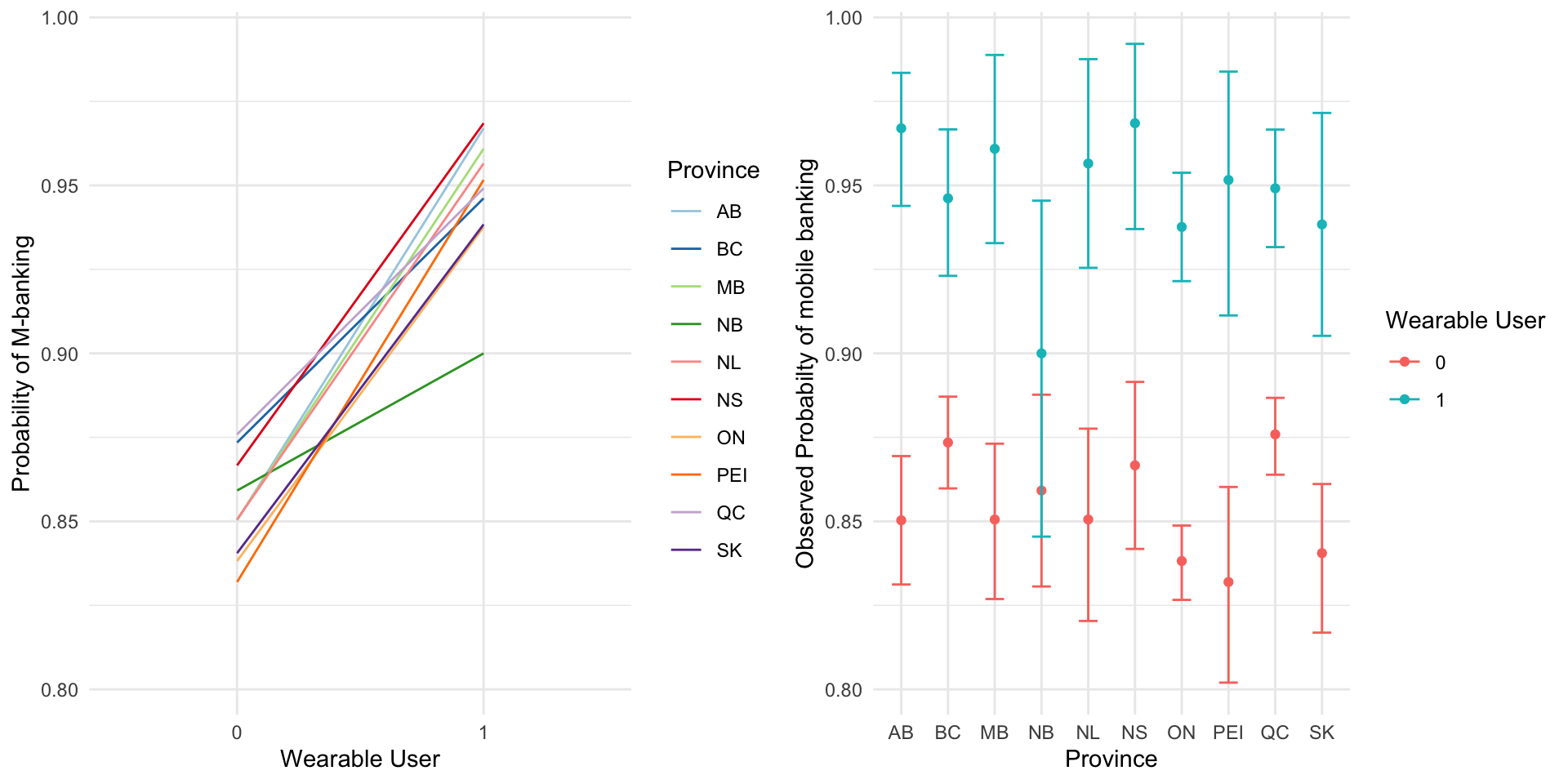

p1 <- ggplot(aes(x = as.factor(isSmartWear), y = MBANK, color = as.factor(PRVNC)), data = wrk_ds) +

stat_summary(fun.data = "mean_cl_boot", geom = 'line', aes(group = as.factor(PRVNC))) +

labs(x = "Wearable User", y = "Probability of M-banking", color = "Province") +

scale_color_brewer(palette = "Paired") +

theme_minimal()

p2 <- ggplot(wrk_ds, aes(as.factor(PRVNC), MBANK, color = as.factor(isSmartWear))) +

stat_summary(fun = mean, geom = "point") +

stat_summary(fun.data = mean_cl_boot, geom = "errorbar", width = 0.4) +

theme_set(theme_bw(base_size = 10)) +

theme(legend.position = "top") +

labs(x = "Province", y = "Observed Probabilty of mobile banking", color = "Wearable User") + theme_minimal()

ggarrange(p1, p2, ncol = 2)

It doesn’t really looks like there’s much grouping happening here! Let’s build the datasets:

wrk_ds <- wrk_ds %>% mutate(

scaled_wtpg = wtpg/max(wtpg)

)wrk_ds_fulldata <- wrk_ds %>% mutate(

# if name has "_f" after it, it's a factor.

# if name has a "_c" after it, it's mean centered.

# if name has no trailing letter, it's just an integer (probably 0-1)

PRVNC_f = as.factor(PRVNC),

SEX_f = factor(SEX,levels = c("0", "1")),

EDU_f = factor(EDU, levels = c("1", "2", "3")),

EDU_c = EDU - mean(EDU),

AGE_f = as.factor(AGE),

AGE_f = relevel(AGE_f, ref = "2"),

AGE_c = AGE - mean(AGE),

INCOME_f = as.factor(INCOME),

INCOME_c = INCOME - mean(INCOME),

EFF_TIME_f = as.factor(EFF_TIME),

# added variables

PSEC_c1 = PSEC - min(PSEC) + 1,

PSEC_c = PSEC - mean(PSEC),

PSEC_scaled = 1 + 7 * ((PSEC - min(PSEC)) / (max(PSEC) - min(PSEC))),

TRST_BANK_f = as.factor(TRST_BANK),

TRST_BANK_f = relevel(TRST_BANK_f, ref = "5"),

TRST_BANK_c = TRST_BANK - mean(TRST_BANK),

USR_TYP = case_when(

isSmartWear == 1 ~ "WEAR",

isSmartWear == 0 ~ "PHON",

.default = "OTHER"

)

)wrk_ds_fulldata_PHON <- wrk_ds_fulldata %>% filter(isSmartWear == 0)

wrk_ds_fulldata_WEAR <- wrk_ds_fulldata %>% filter(isSmartWear == 1) Let’s see the counts for the groups:

ctab <- table(wrk_ds_fulldata$MBANK, wrk_ds_fulldata$USR_TYP)

ctab

PHON WEAR

0 2214 169

1 13174 2995A simple \chi^2 test shows these users are significantly different in how they m-bank:

chisq.test(ctab)

Pearson's Chi-squared test with Yates' continuity correction

data: ctab

X-squared = 191.04, df = 1, p-value < 2.2e-16Summary Statistics of the dataset:

psycDescribe <- psych::describe(

wrk_ds_fulldata %>% dplyr::select(isSmartWear, AGE, SEX, EDU, INCOME, EFF_TIME, TRST_BANK, PSEC) #if it's numeric.

)

psycDescribe <- as.data.frame(psycDescribe)

gt(psycDescribe)| vars | n | mean | sd | median | trimmed | mad | min | max | range | skew | kurtosis | se |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 18552 | 1.705476e-01 | 0.3761234 | 0.0000000 | 0.08819566 | 0.000000 | 0.000000 | 1.000000 | 1.000000 | 1.75173699 | 1.0686401 | 0.002761436 |

| 2 | 18552 | 4.117400e+00 | 1.5025952 | 4.0000000 | 4.20165746 | 1.482600 | 1.000000 | 6.000000 | 5.000000 | -0.31941695 | -1.0076646 | 0.011031806 |

| 3 | 18552 | 5.211837e-01 | 0.4995645 | 1.0000000 | 0.52647891 | 0.000000 | 0.000000 | 1.000000 | 1.000000 | -0.08480409 | -1.9929157 | 0.003667720 |

| 4 | 18552 | 2.151951e+00 | 0.7866826 | 2.0000000 | 2.18993397 | 1.482600 | 1.000000 | 3.000000 | 2.000000 | -0.27452999 | -1.3370776 | 0.005775694 |

| 5 | 18552 | 3.230972e+00 | 1.3482437 | 3.0000000 | 3.28870772 | 1.482600 | 1.000000 | 5.000000 | 4.000000 | -0.19217593 | -1.1623489 | 0.009898583 |

| 6 | 18552 | 5.085705e-01 | 0.4999400 | 1.0000000 | 0.51071284 | 0.000000 | 0.000000 | 1.000000 | 1.000000 | -0.03428428 | -1.9989323 | 0.003670477 |

| 7 | 18552 | 3.710921e+00 | 0.9637567 | 4.0000000 | 3.80083547 | 1.482600 | 1.000000 | 5.000000 | 4.000000 | -0.68270585 | 0.3415415 | 0.007075743 |

| 8 | 18552 | 2.573285e-17 | 0.8816774 | 0.1028678 | 0.03752289 | 1.053947 | -1.529966 | 1.302335 | 2.832302 | -0.30718042 | -1.0974666 | 0.006473130 |

Modeling

First, since there’s clustering on provinces, I run a fixed effect model and test it against a simple logistic regression to see if there is a grouping effect. First of all, the model fails to converge -

model_full_fixedeffect <- glmer(

MBANK ~ AGE_f + SEX_f + EDU_f + INCOME_f + EFF_TIME_f + TRST_BANK_f + PSEC + (1 | PRVNC),

data = wrk_ds_fulldata,

family = binomial,

weights = scaled_wtpg

)Warning :non-integer #successes in a binomial glm!

Warning :failure to converge in 10000 evaluations

Warning :convergence code 4 from Nelder_Mead: failure to converge in 10000 evaluations

Warning :unable to evaluate scaled gradient

Warning :Model failed to converge: degenerate Hessian with 1 negative eigenvalues

model_full <- glm(

MBANK ~ AGE_f + SEX_f + EDU_f + INCOME_f + EFF_TIME_f + TRST_BANK_f + PSEC,

data = wrk_ds_fulldata,

family = quasibinomial,

weights = scaled_wtpg

)The LR test shows that there is no improvement to the model, so going with the simpler model is better.

lrtest(model_full, model_full_fixedeffect)| #DF | LogLik | Df | Chisq | Pr(>Chisq) |

|---|---|---|---|---|

| 19 | ||||

| 20 | -27.041 | 1 |

The mathematical formulations of all three models follows this:

\begin{equation*} \begin{split} & logit(MBANK) = \\ & \hspace{1cm} \beta_0 + \beta_1 \ AGE_1 \ + \beta_2 \ AGE_3 \ + \beta_3 \ AGE_4 \ + \beta_4 \ AGE_5 \ + \beta_5 \ AGE_6 \ + \\ & \hspace{1cm} \beta_6 \ SEX_F \ + \beta_7 \ EDU_2 \ + \beta_8 \ EDU_3 \ + \beta_{9} \ INCOME_2 \ + \beta_{10} \ INCOME_3 \ + \\ & \hspace{1cm} \beta_{11} \ INCOME_4 \ + \beta_{12} \ INCOME_5 \ + \beta_{13} \ EFF\_TIME \ + \beta_{14} \ TRST\_BANK_1 \ + \\ & \hspace{1cm} \beta_{15} \ TRST\_BANK_2 \ + \beta_{16} \ TRST\_BANK_3 \ + \beta_{17} \ TRST\_BANK_4 \ + \beta_{18} \ PSEC \ + \epsilon \\ \end{split} \end{equation*}

The only difference is the dataset each is coming from. I do need to calculate the robust cluster standard errors for more accurate results:

model_full_cluster_se <- vcovCL(model_full, cluster = wrk_ds_fulldata$PRVNC)

# summary table of results

model_full_summary_clustered <- coeftest(model_full, vcov = model_full_cluster_se)

# PHON-only

model_phon <- glm(

MBANK ~ AGE_f + SEX_f + EDU_f + INCOME_f + EFF_TIME_f + TRST_BANK_f + PSEC,

data = wrk_ds_fulldata_PHON,

family = quasibinomial,

weights = scaled_wtpg

)

model_phon_cluster_se <- vcovCL(model_phon, cluster = wrk_ds_fulldata_PHON$PRVNC)

model_phon_summary_clustered <- coeftest(model_phon, vcov = model_phon_cluster_se)

# WEAR-only

model_wear <- glm(

MBANK ~ AGE_f + SEX_f + EDU_f + INCOME_f + EFF_TIME_f + TRST_BANK_f + PSEC,

data = wrk_ds_fulldata_WEAR,

family = quasibinomial,

weights = scaled_wtpg

)

model_wear_cluster_se <- vcovCL(model_wear, cluster = wrk_ds_fulldata_WEAR$PRVNC)

model_wear_summary_clustered <- coeftest(model_wear, vcov = model_wear_cluster_se)Using textreg (in my original R markdown file, and htmlreg here for website preview) to produce \LaTeX code for the table:

screenreg(

list(model_full_summary_clustered, model_phon_summary_clustered, model_wear_summary_clustered),

custom.model.names = c("Full Data (coeff)",

"Phone Only (coeff)",

"WEAR Only (coeff)")

)

======================================================================

Full Data (coeff) Phone Only (coeff) WEAR Only (coeff)

----------------------------------------------------------------------

(Intercept) 1.83 *** 1.95 *** 1.23 **

(0.16) (0.20) (0.39)

AGE_f1 -1.01 *** -1.12 *** -0.25

(0.05) (0.11) (0.25)

AGE_f3 0.02 -0.06 0.52 **

(0.10) (0.12) (0.16)

AGE_f4 -0.03 -0.12 1.00

(0.13) (0.18) (0.52)

AGE_f5 -0.09 -0.13 0.16

(0.17) (0.20) (0.30)

AGE_f6 -0.23 -0.29 0.39

(0.13) (0.15) (0.35)

SEX_f1 0.11 ** 0.09 *** 0.16

(0.03) (0.02) (0.27)

EDU_f2 0.32 *** 0.25 *** 1.02 ***

(0.07) (0.05) (0.29)

EDU_f3 0.47 *** 0.42 *** 0.94 ***

(0.02) (0.03) (0.22)

INCOME_f2 0.15 * 0.20 * -0.51

(0.07) (0.09) (0.35)

INCOME_f3 0.20 * 0.21 * -0.03

(0.09) (0.10) (0.28)

INCOME_f4 0.43 *** 0.42 *** 0.19

(0.12) (0.12) (0.42)

INCOME_f5 0.59 *** 0.60 *** 0.16

(0.10) (0.15) (0.44)

EFF_TIME_f1 0.56 *** 0.54 *** 0.69 *

(0.05) (0.04) (0.33)

TRST_BANK_f1 -1.44 *** -1.53 *** -0.00

(0.18) (0.17) (0.59)

TRST_BANK_f2 -0.69 *** -0.67 *** -0.66 ***

(0.17) (0.18) (0.19)

TRST_BANK_f3 -0.67 *** -0.73 *** -0.29

(0.13) (0.12) (0.19)

TRST_BANK_f4 -0.11 -0.16 0.31

(0.12) (0.09) (0.40)

PSEC 0.93 *** 0.94 *** 0.70 ***

(0.05) (0.04) (0.09)

======================================================================

*** p < 0.001; ** p < 0.01; * p < 0.05The R code to generate \LaTeX code:

texreg(

list(model_full_summary_clustered,

model_phon_summary_clustered,

model_wear_summary_clustered),

custom.model.names = c("Full Data", "Phone-Only", "Wear-Only"),

digits = 3,

stars = c(0.001, 0.01, 0.05), # Significance levels for stars

single.row = FALSE, # Standard errors in parentheses below coefficients

custom.note = "Significance levels: *p < 0.05; **p < 0.01; ***p < 0.001",

booktabs = TRUE, # Use booktabs-style formatting

caption = "Logistic Regression Results with Robust Standard Errors"

)Analysis of Results

Since the point it to compare the values for coefficients in each model, I will need to perform wald test. It’s essentially just a Z statistic calculation. Let’s consider \hat{\beta_{p1}} the estimated coefficient of variable 1 from the PHON only model and \hat{beta_{w1}} the same variable’s estimate coefficient in WEAR only model. I want to know, is the difference between the two significantly different from zero? That is, H_0: \hat{\beta_{p1}} - \hat{\beta_{w1}} = 0. If I reject H_0, that means they’re significantly different. The statistic is calculated as the ratio of the estimate (difference) over the standard error the estimate (difference): Z = \frac{\hat{\beta_{p1}} - \hat{\beta_{w1}}}{\sqrt{\sigma_{\beta_{p1}} + \sigma_{\beta_{w1}}}}

calc_wald_test <- function(model1, model2, variable_name){

coeff1 <- model1[variable_name, 1]

coeff2 <- model2[variable_name, 1]

se1 <- model1[variable_name, 2]

se2 <- model1[variable_name, 2]

diff <- coeff1 - coeff2

se_diff <- sqrt(se1^2 + se2^2)

z <- diff / se_diff

p <- 2 * (1 - pnorm(abs(z)))

res <- c(z = z, p = p)

return(res)

}Here’s how you do this:

- Get the results for FullData vs PHON

- Get the results for FullData vs WEAR

- Get the results for PHON vs WEAR

coefs_ <- c('AGE_f1', 'AGE_f3','AGE_f4','AGE_f5','AGE_f6',

'SEX_f1',

'EDU_f2','EDU_f3',

'INCOME_f2','INCOME_f3','INCOME_f4','INCOME_f5',

'EFF_TIME_f1',

'TRST_BANK_f1','TRST_BANK_f2','TRST_BANK_f3','TRST_BANK_f4',

'PSEC')

results <- c()

# Loop through coefficients and format results

for (coef_ in coefs_) {

full_vs_phone <- calc_wald_test(model_full_summary_clustered, model_phon_summary_clustered, coef_)

full_vs_wear <- calc_wald_test(model_full_summary_clustered, model_wear_summary_clustered, coef_)

phone_vs_wear <- calc_wald_test(model_phon_summary_clustered, model_wear_summary_clustered, coef_)

## Check significance (if p > 0.05, set as "no", otherwise keep z-score)

# the dollar signs and ^{} are because I wanted to copy paste the results into LaTeX overleaf ! IGNORE

full_vs_phone_text <- paste0("$ ", round(full_vs_phone["z"], 3), "^{} $ & ", " $ ", round(full_vs_phone["p"], 3), "$")

full_vs_wear_text <- paste0("$ ", round(full_vs_wear["z"], 3), "^{} $ & ", " $ ", round(full_vs_wear["p"], 3), "$")

phone_vs_wear_text <- paste0("$ ", round(phone_vs_wear["z"], 3), "^{} $ & ", " $ ", round(phone_vs_wear["p"], 3), "$")

# Format the result for this coefficient

# again, the &'s are for overleaf / LaTeX convenience

result <- paste0(

full_vs_phone_text, " & ",

full_vs_wear_text, " & ",

phone_vs_wear_text

)

# Append to results list

results <- c(results, result)

}

# Print the results

for (res in results) {

print(res)

}[1] "$ 1.485^{} $ & $ 0.137$ & $ -10.352^{} $ & $ 0$ & $ -5.625^{} $ & $ 0$"

[1] "$ 0.555^{} $ & $ 0.579$ & $ -3.413^{} $ & $ 0.001$ & $ -3.48^{} $ & $ 0.001$"

[1] "$ 0.46^{} $ & $ 0.646$ & $ -5.48^{} $ & $ 0$ & $ -4.488^{} $ & $ 0$"

[1] "$ 0.142^{} $ & $ 0.887$ & $ -1.072^{} $ & $ 0.284$ & $ -1.038^{} $ & $ 0.299$"

[1] "$ 0.33^{} $ & $ 0.742$ & $ -3.488^{} $ & $ 0$ & $ -3.159^{} $ & $ 0.002$"

[1] "$ 0.493^{} $ & $ 0.622$ & $ -1.138^{} $ & $ 0.255$ & $ -2.363^{} $ & $ 0.018$"

[1] "$ 0.698^{} $ & $ 0.485$ & $ -6.641^{} $ & $ 0$ & $ -10.406^{} $ & $ 0$"

[1] "$ 1.5^{} $ & $ 0.134$ & $ -13.742^{} $ & $ 0$ & $ -12.788^{} $ & $ 0$"

[1] "$ -0.525^{} $ & $ 0.6$ & $ 6.484^{} $ & $ 0$ & $ 5.403^{} $ & $ 0$"

[1] "$ -0.069^{} $ & $ 0.945$ & $ 1.932^{} $ & $ 0.053$ & $ 1.658^{} $ & $ 0.097$"

[1] "$ 0.071^{} $ & $ 0.943$ & $ 1.456^{} $ & $ 0.145$ & $ 1.351^{} $ & $ 0.177$"

[1] "$ -0.063^{} $ & $ 0.95$ & $ 3.013^{} $ & $ 0.003$ & $ 2.13^{} $ & $ 0.033$"

[1] "$ 0.382^{} $ & $ 0.702$ & $ -1.923^{} $ & $ 0.054$ & $ -2.489^{} $ & $ 0.013$"

[1] "$ 0.361^{} $ & $ 0.718$ & $ -5.769^{} $ & $ 0$ & $ -6.453^{} $ & $ 0$"

[1] "$ -0.071^{} $ & $ 0.943$ & $ -0.141^{} $ & $ 0.888$ & $ -0.065^{} $ & $ 0.948$"

[1] "$ 0.287^{} $ & $ 0.774$ & $ -2.181^{} $ & $ 0.029$ & $ -2.682^{} $ & $ 0.007$"

[1] "$ 0.301^{} $ & $ 0.763$ & $ -2.475^{} $ & $ 0.013$ & $ -3.559^{} $ & $ 0$"

[1] "$ -0.19^{} $ & $ 0.849$ & $ 3.546^{} $ & $ 0$ & $ 4.524^{} $ & $ 0$"Bonus Visualizations

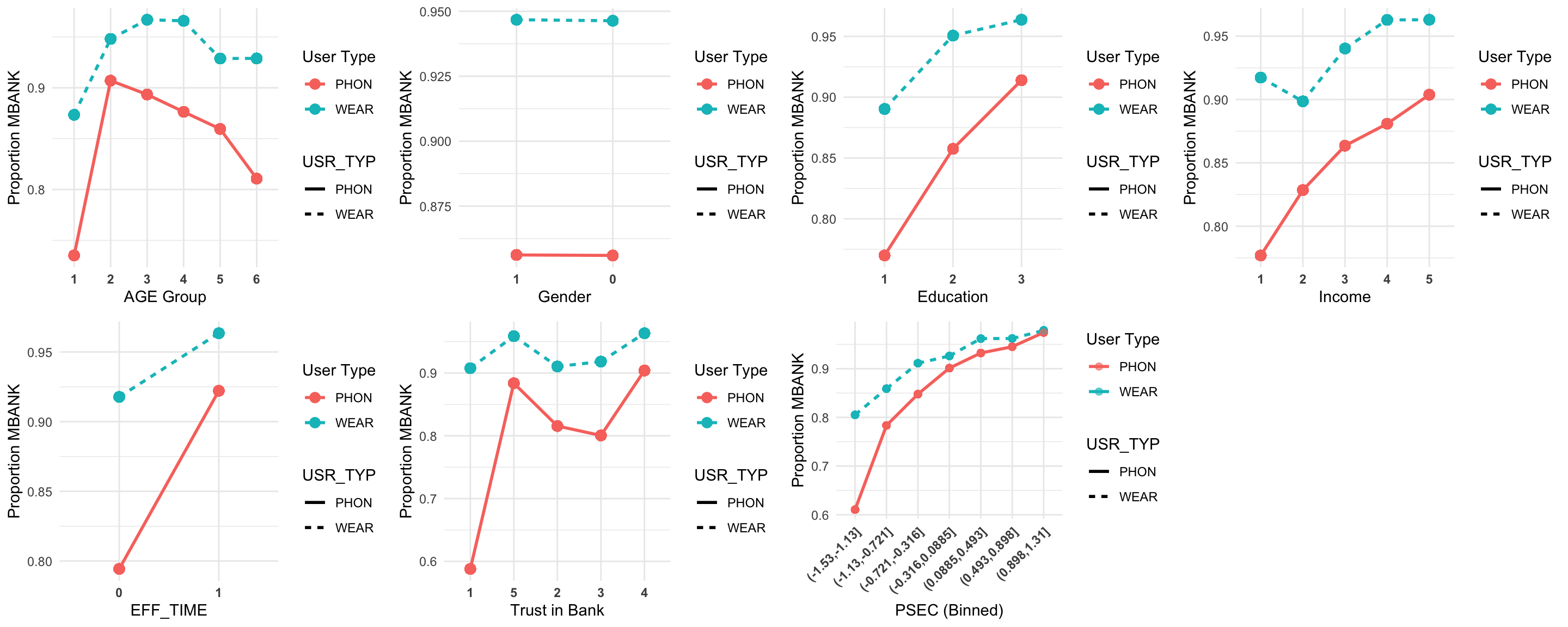

age_gg <- ggplot(wrk_ds_fulldata %>%

group_by(AGE_f, USR_TYP) %>%

mutate(Proportion_mbank = mean(MBANK)),

aes(x = relevel(AGE_f, ref = "1"), y = Proportion_mbank, color = USR_TYP, group = USR_TYP, linetype = USR_TYP)) +

geom_line(size = 1) +

geom_point(size = 3) +

labs(

x = "AGE Group",

y = "Proportion MBANK",

color = "User Type"

) +

theme_minimal() + theme(strip.text = element_text(size = 12, face = "bold"), axis.text.x = element_text(face = "bold"))

sex_gg <- ggplot(wrk_ds_fulldata %>%

group_by(SEX_f, USR_TYP) %>%

mutate(Proportion_mbank = mean(MBANK)),

aes(x = relevel(SEX_f, ref = "1"), y = Proportion_mbank, color = USR_TYP, group = USR_TYP, linetype = USR_TYP)) +

geom_line(size = 1) +

geom_point(size = 3) +

labs(

x = "Gender",

y = "Proportion MBANK",

color = "User Type"

) +

theme_minimal() + theme(strip.text = element_text(size = 12, face = "bold"), axis.text.x = element_text(face = "bold"))

edu_gg <- ggplot(wrk_ds_fulldata %>%

group_by(EDU_f, USR_TYP) %>%

mutate(Proportion_mbank = mean(MBANK)),

aes(x = EDU_f, y = Proportion_mbank, color = USR_TYP, group = USR_TYP, linetype = USR_TYP)) +

geom_line(size = 1) +

geom_point(size = 3) +

labs(

x = "Education",

y = "Proportion MBANK",

color = "User Type"

) +

theme_minimal() + theme(strip.text = element_text(size = 12, face = "bold"), axis.text.x = element_text(face = "bold"))

trst_gg <- ggplot(wrk_ds_fulldata %>%

group_by(TRST_BANK_f, USR_TYP) %>%

mutate(Proportion_mbank = mean(MBANK)),

aes(x = relevel(TRST_BANK_f, ref = "1"), y = Proportion_mbank, color = USR_TYP, group = USR_TYP, linetype = USR_TYP)) +

geom_line(size = 1) +

geom_point(size = 3) +

labs(

x = "Trust in Bank",

y = "Proportion MBANK",

color = "User Type"

) +

theme_minimal() + theme(strip.text = element_text(size = 12, face = "bold"), axis.text.x = element_text(face = "bold"))

sec_gg <- ggplot(wrk_ds_fulldata %>%

mutate(PSECBIN = cut(PSEC, breaks = 7)) %>%

group_by(PSECBIN, USR_TYP) %>%

mutate(Proportion_mbank = mean(MBANK)),

aes(x = PSECBIN, y = Proportion_mbank, color = USR_TYP, group = USR_TYP, linetype = USR_TYP)) +

geom_line(size = 1) +

geom_point(size = 2, alpha = 0.6) +

labs(

x = "PSEC (Binned)",

y = "Proportion MBANK",

color = "User Type"

) +

theme_minimal() + theme(strip.text = element_text(size = 12, face = "bold"), axis.text.x = element_text(face = "bold", angle = 45, hjust = 1))

income_gg <- ggplot(wrk_ds_fulldata %>%

group_by(INCOME_f, USR_TYP) %>%

mutate(Proportion_mbank = mean(MBANK)),

aes(x = INCOME_f, y = Proportion_mbank, color = USR_TYP, group = USR_TYP, linetype = USR_TYP)) +

geom_line(size = 1) +

geom_point(size = 3) +

labs(

x = "Income",

y = "Proportion MBANK",

color = "User Type"

) +

theme_minimal() + theme(strip.text = element_text(size = 12, face = "bold"), axis.text.x = element_text(face = "bold"))

eff_gg <- ggplot(wrk_ds_fulldata %>%

group_by(EFF_TIME_f, USR_TYP) %>%

mutate(Proportion_mbank = mean(MBANK)),

aes(x = EFF_TIME_f, y = Proportion_mbank, color = USR_TYP, group = USR_TYP, linetype = USR_TYP)) +

geom_line(size = 1) +

geom_point(size = 3) +

labs(

x = "EFF_TIME",

y = "Proportion MBANK",

color = "User Type"

) +

theme_minimal() + theme(strip.text = element_text(size = 12, face = "bold"), axis.text.x = element_text(face = "bold"))

ggarrange(age_gg, sex_gg, edu_gg, income_gg, eff_gg, trst_gg, sec_gg,

ncol = 4, nrow = 2)